In the last few days, Paul Krugman has been particularly outspoken in asserting that austerity has failed but also that Keynesian economics has won. Is he right? I don’t think so.

It seems fair to describe the Obama administration’s stimulus as based on Keynesian economics theory — the idea that during a recession, the government should spend money in order to prop up aggregate demand. But the country’s economic performance of the last four or five years can hardly be described has a rousing success for Keynesian economics, at least as implemented by the administration. In fact, measured by the unemployment rate, it hasn’t been a success by the administration’s own standards.

To that, Krugman says that the stimulus implemented by the administration wasn’t big enough and, as such, that Keynesian economics hasn’t been tried yet. According to him, with interest rates at or near zero (and in what he would describe as a liquidity trap), monetary policy alone couldn’t have jump-started the economy, and much more stimulus (i.e. spending) was needed to prop up aggregate demand. According to Krugman, Keynesian economics haven’t really been tried, and that’s why the economy is doing poorly; if we had tried it, we’d be doing better. So Keynesianism survives unscathed. But by this logic, free-market economics is doing pretty well, too: I think we can all agree that free-market economics wasn’t tried. The economy hasn’t really recovered properly. This must mean free-market economics has won.

The debate between Keynesians and free-market economists has been going on for decades, if not longer. The main reason for the dispute’s longevity is that macroeconomics is far from simple. For one thing, for any one condition, there are multiple plausible causal factors and there are no controlled experiments. These limitations, sadly, are unlike to change anytime soon, and as such we should expect that the debate will be going on for many more years, in spite of Krugman’s victory lap.

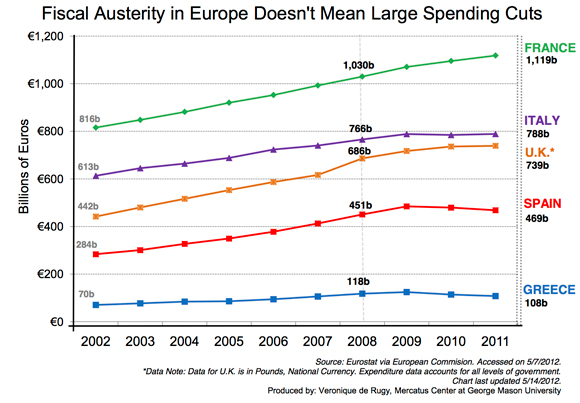

Now, let’s turn to the question of austerity. It is a sad fact that austerity, as defined by economists, represents the measures implemented by a government in order to reduce the debt-to-GDP ratio. Unlike Keynesians, I do not think that debt is good for economic growth, but I would prefer the word “austerity” to describe the measures implemented to skrink the size and scope of government, rather than improve a government’s fiscal situation. Besides, defining austerity as an attempt to reduce the debt leads to a lot of confusions, because it can take different forms — cutting spending, raising taxes, or a mix of both. Why does this matter? Because the different types of austerity measures produce very different results. In other words, the important question about austerity has less to do with the size of the austerity package than what type of austerity measures are implemented.

In a recent paper with Harvard economist Alberto Alesina, we show that the consensus in the academic literature is that the composition of fiscal adjustment, or what economists call austerity (deficit and debt reduction) is a key factor in achieving successful and lasting reductions in debt-to-GDP ratio. The general consensus: Fiscal-adjustment packages made mostly of spending cuts are more likely to lead to lasting debt reduction than those made of tax increases.

There is still significant debate about the short-term economic impact of fiscal adjustments. However, as we show in our paper, important lessons have emerged. For instance, while fiscal adjustments may not always have an immediate, clear economic effect, spending-based adjustments are much less costly in terms of output than tax-based ones. In fact, when governments try to reduce the debt by raising taxes, it is likely to result in deep and pronounced recessions, possibly making the fiscal adjustment counterproductive. We also discuss how fiscal adjustment is more likely to be good for economic growth (“expansionary”) when it’s accompanied by growth-oriented policies, such as liberalizing both labor markets and other markets and a monetary policy that keeps interest rates low.

{kind=link}