The Congressional Budget Office (CBO) released its annual “Budget and Economic Outlook” on February 7, 2024. I figured it is never too late to let you know that we will be drowning in deficit and debt for the next ten years.

- Outlays rise from 23.1 percent in 2024 to 24.1 percent of GDP in 2034.

- Revenues grow from $4.9 trillion in 2024 to $7.4 in 2034.

- Gross debt is going up to $54.3 trillion in 2034, from $34.8 in 2024.

- Deficits equal or exceed 5.2 percent of GDP in every year from 2024 to 2034. The past-50-year average was 3.7 percent.

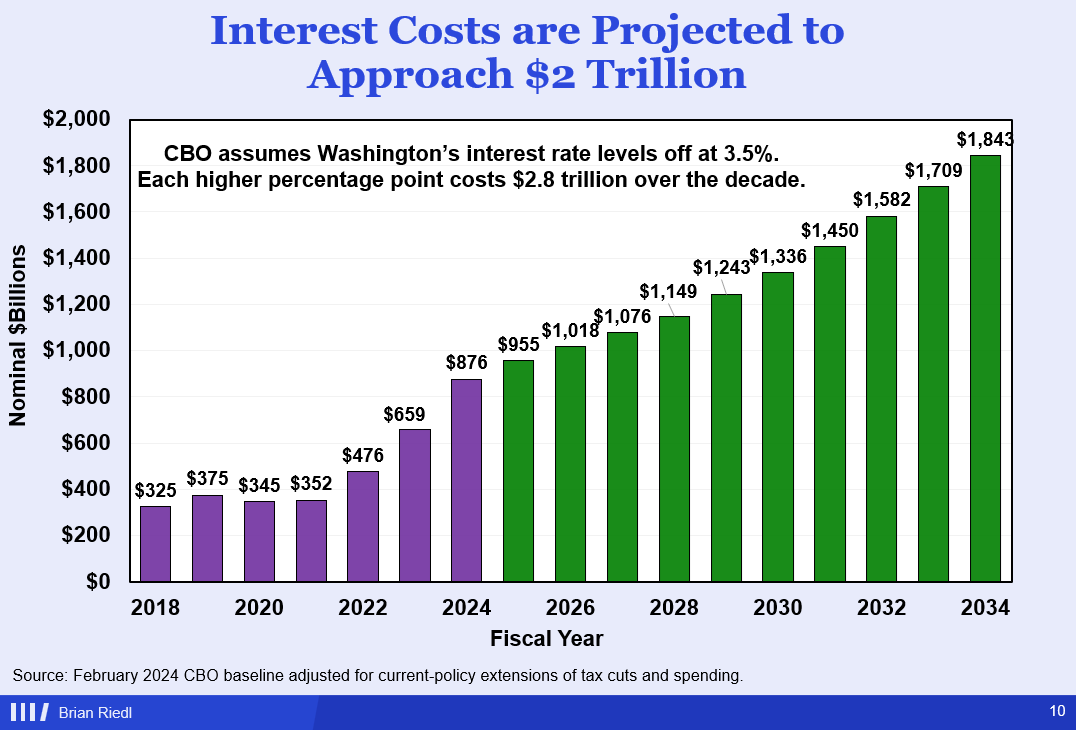

- Interest payments are a majority of the deficit in the next ten years.

There are a few things worth noting. CBO is required to score the current policy baseline.* That’s important because there are a few things as projected by CBO (again, because it has no choice) that are unrealistic. Brian Riedl sums them up well:

-

All 2017 tax cuts (+ recent ACA expansion) expire on schedule.

-

Congress cuts discretionary spending to 5.1% of GDP — the lowest level since the 1930s.

No Chance. Fix those, and baseline budget deficit jumps to $3.6 trillion

Matt Dickerson at EPIC notes that the 2024 deficit will be much higher than what CBO projects:

Legislation currently under consideration would add billions to the deficit, including:

- The Johnson-Schumer side deal to increase discretionary spending above the levels specified in the Fiscal Responsibility Act would add about $40 billion in un-offset discretionary spending above the baseline.

- The Senate supplemental appropriations bill currently under consideration would add $118 billion in higher discretionary spending.

- The Smith-Wyden tax legislation that recently passed the House would increase FY 2024 spending by $3.6 billion and reduce revenues by $113.9 billion.

That is about $275 billion in potentially higher FY 2024 deficits above CBO’s baseline (assuming the additional discretionary appropriations are expended this year).

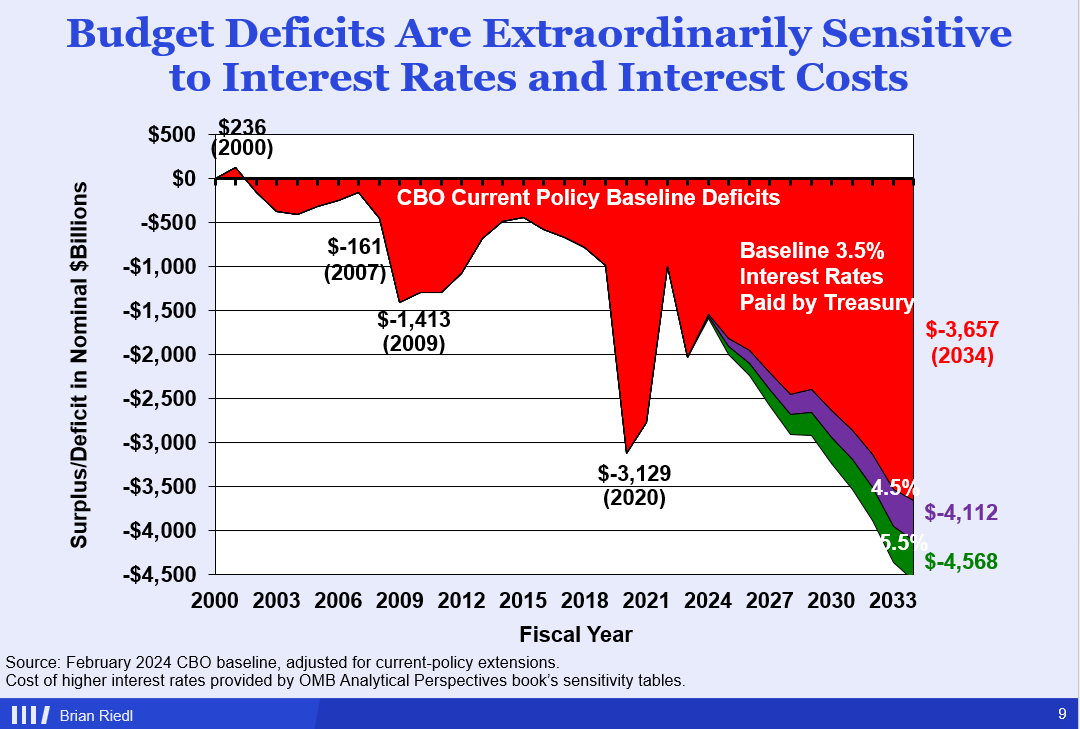

CBO is also assuming that the Department of the Treasury can sell more than $10 trillion in bonds (most of it is rolling over maturing debt) year after year and that it will pay 3.5 percent interest on its debt within a decade. If that number goes up to 4.5 percent, it will add $2.8 trillion to the deficit over those ten years.

From Riedl:

And:

There is an enormous fiscal challenge coming our way. It starts in 2025 with the expiration of major provisions of the 2017 tax cuts, the reinstatement of the debt ceiling, the end of Fiscal Responsibility Act discretionary-spending limits, and the reinforcement of Statutory PAYGO. Then, within the next decade, Social Security and Medicare will face insolvency.

A growing number of conservatives are in favor of new or increased family benefits and/or workers’ benefits. We can have debates about the value of these specific proposals and their impact on the incentive to marry or to work. However, no one who argues for more spending should be able to make their case without also naming the programs they would like to cut first.

That’s unless you believe that inflation, debt crises, or low growth are good for families and workers.

* With the exception of what happens when the Social Security and Medicare Trust Funds “dry out.” In this case, Congress instructed CBO to pretend general revenues will be used to pay all the benefits. That won’t happen without action from Congress.