The annual reports of the Social Security and Medicare trustees were released yesterday. As always, the reports present a grim and deteriorating picture of the two programs’ financial outlooks. Here are a few highlights:

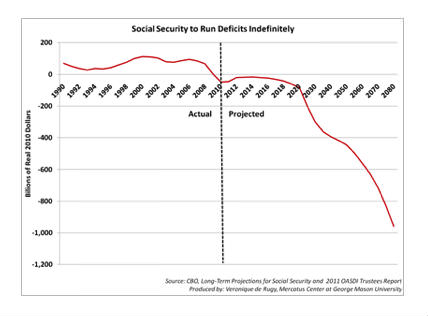

1) Since 2010 Social Security has been running a permanent cash-flow deficit. That means that taxes collected for the program aren’t enough to cover the benefits paid to retirees. To fill the gap, the program is drawing from the trust-fund balances (first using the interest, then the principal) to keep payments to retirees going; in concrete terms, Treasury will borrow money to pay back the trust funds.

2) Obviously, the gap between the tax collection and the benefits paid is getting wider as Congress keeps extending the payroll-tax cut and filling the trust fund with borrowed money. If anything, this gap is exposing the fiction that we are all paying for the benefits that we will get and that, as a result, we can’t reform the program because we have paid for the benefits. According to my colleague Jason Fichtner, there are ways to put the trust fund back on solid grounds: You can increase the payroll-tax rate from its usual 12.4 percent to 15.1 percent, cut benefits by 16.2 percent, or some combination of both. Modest reforms like increasing the eligibility age would achieve that goal too. Extending the payroll-tax cut only aggravates the problem for those who want to preserve the program as it is now.

{kind=link}

3) The Social Security trust fund will be exhausted by 2035 — a year sooner than was projected last year. The combined retirement and disability trust funds will be exhausted by 2033 — that’s three years sooner than was predicted last year.

It matters because the trust fund determines the spending authority of the program. That means that without a positive balance in the trust fund, the program won’t have the authority to pay out full benefits, but only what the program collects in taxes — which means a cut in benefits across the board.

#more#4) The Medicare Hospital Insurance trust fund will run out of assets in 2024, as projected last year. Remember that the Affordable Care Act (ACA) was supposed to push back the insolvency date of the program from 2017 to 2029. This is not happening. The HI trust fund, like the SS one, determines the spending authority of the programs. Without a positive balance in the HI trust fund, the program won’t have the authority to pay out all benefits, just what the program collects in taxes. (Medicare HI gets some income from premiums and from payments by states.) However, recent increases in health-care costs are likely to exhaust the trust fund way sooner than projected this year. The drop will likely be seen in the next Trustees’ report.

5) As was the case in the past, even these grim numbers should be taken with a grain of salt. First, some of the projected revenue from the ACA may not materialize. The demise of the CLASS Act provides a good example of a revenue-booster policy that won’t be raising money after all. Also, many projected savings in the ACA are unlikely to materialize. For instance, the chief actuary of the program, Richard Foster, explains at the end of the Trustees’s Report (p. 277): “Current law would require a physician fee reduction of an estimated 30.9 percent on January 1, 2013 — an implausible expectation.”

Foster raises further factors that explain why we shouldn’t expect cost-reduction aspects of the law to materialize:

Specifically, the annual price updates for most categories of non-physician health services will be adjusted downward each year by the growth in economy-wide productivity. The best available evidence indicates that most health care providers cannot improve their productivity to this degree—or even approach such a level—as a result of the labor-intensive nature of these services.

Without unprecedented changes in health care delivery systems and payment mechanisms, the prices paid by Medicare for health services are very likely to fall increasingly short of the costs of providing these services. By the end of the long-range projection period, Medicare prices for hospital, skilled nursing facility, home health, hospice, ambulatory surgical center, diagnostic laboratory, and many other services would be less than half of their level under the prior law.

He concludes:

For these reasons, the financial projections shown in this report for Medicare do not represent reasonable expectation for actual program operations in either the short range (as a result of the unsustainable reductions in physician payment rates) or the long range (because of the strong likelihood that the statutory reductions in price updates for most categories of Medicare provider services will not be viable).

For alternatives to the spending path of the program, look at the chart provided on p. 220 of the report.

Furthermore, Avik Roy had an interesting piece over at the Apothecary blog showing that Medicare will actually be in the red starting, not in 2024 but in 2016 (if not sooner). This date is based on the Centers for Medicare and Medicaid Services’ findings. He also explains how the Trustees manage to reconcile both dates (2024 and 2016):

The Trustees, by saying that Medicare will go bankrupt in 2024, instead of 2016, are simultaneously saying that the program will increase the deficit by several hundred billion dollars. This is precisely the insight that Charles Blahous, one of the Medicare Trustees, explained in his recent report on the program.

Think of it this way: if supporters of the Affordable Care Act came clean, they would say one of two things: (1) Medicare is going bankrupt in 2016, but the CBO scores the ACA as deficit neutral; or (2) Medicare is going bankrupt in 2024, and Blahous’ score of the ACA as increasing the deficit by $300-500 billion is accurate.

His whole piece is here and it contains many relevant links.

6) The Disability Insurance trust fund will be insolvent by 2016 — two years earlier than was predicted last year. For years it has been clear that this program is highly dysfunctional and isn’t financially sound.

Now what? It shouldn’t matter where you are on the political spectrum. At this point, it should be clear that the financial outlook for Social Security and Medicare is bad if we do not change course. Reforms are needed. The longer Congress delays dealing with the Medicare/Medicaid and Social Security problems, the worse the shock will be.

I would prefer moving away from this “entitlement” system where everyone gets something from the government (after being forced to pay for part of it — part being the relevant word here) and shift to a true safety net where we take care of poor people (that could mean a better Medicaid and no Medicare). However, there are many other options to address our problems. The only certainly bad option is to continue doing nothing.